- DATE:

- AUTHOR:

- S&P Global

March 2026 S&P Capital IQ Release Notes

S&P Capital IQ Release Highlights

In this release, we added new enhancements on Capital IQ to improve your daily workflows:

Portfolio Analytics: Introduced group-level what-if analysis, enhanced folder management, and new MSCI classifications, enabling users to quickly test allocation changes, stay organized as usage scales, and gain deeper geographic and market-level insights.

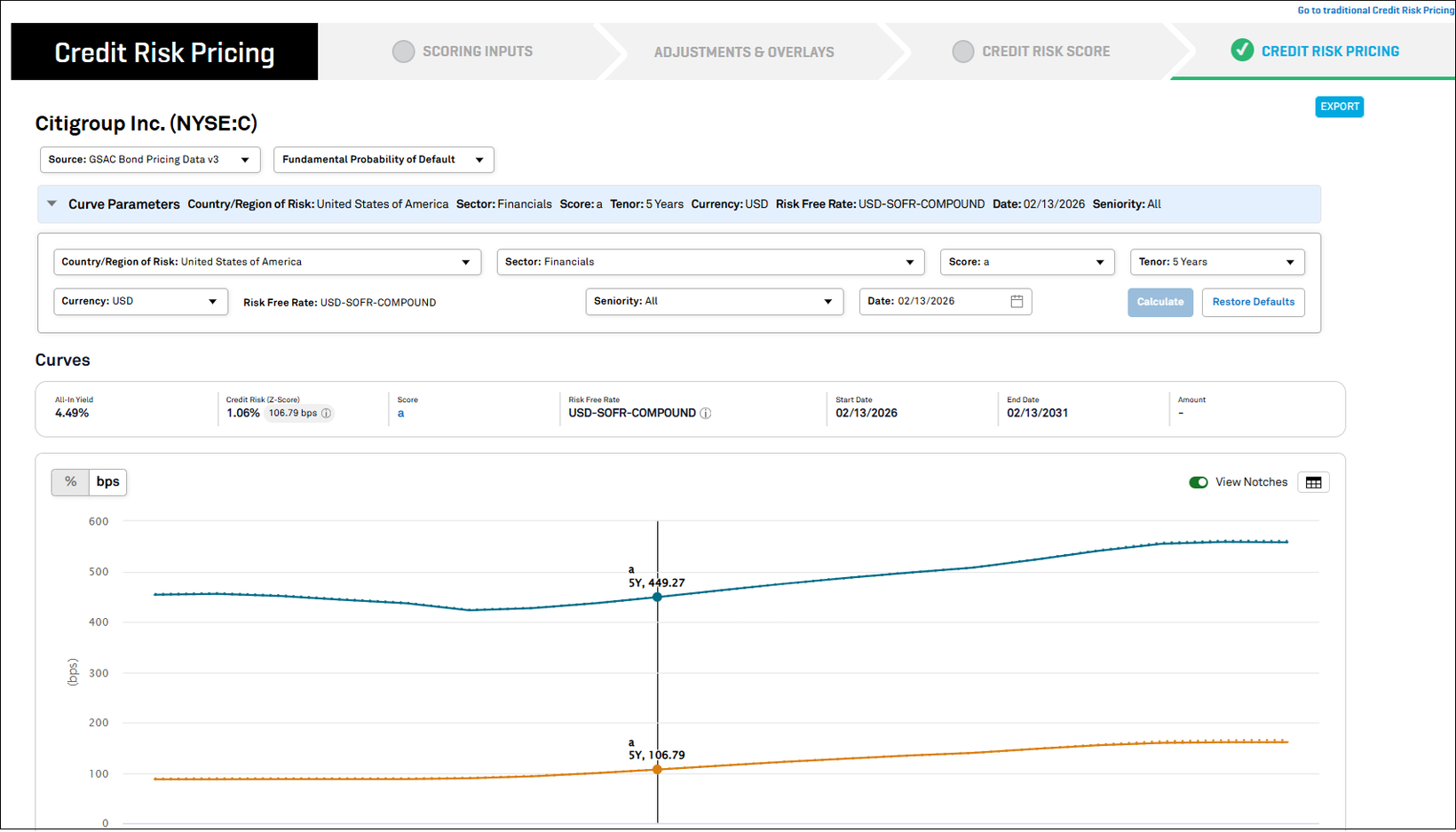

Credit Risk Pricing: Enhanced GSAC v3-centered interface streamlines transfer pricing analysis with unified inputs and outputs, dynamic parameter selection, and seamless access to current and historical methodologies, delivering greater structure and consistency.

S&P Capital IQ Plug-In: EWS 1.0 in the S&P Capital IQ Plug-In introduces early warning signals to alert users of a company’s declining risk level.

Portfolio Analytics

In this release, we expanded Portfolio Analytics with ‘group-level what-if analysis’, enhanced folder management, and new MSCI classifications. These updates help users quickly test allocation changes, stay organized as usage scales, and gain deeper geographic and market-level insights.

Group-Level What-If Analysis

Users can now perform ‘what-if analysis’ at the grouping level – such as sector, industry, or region – in addition to adjusting individual holdings. This enables faster evaluation of allocation changes, while preserving total portfolio market value.

Key Capabilities:

Run what-if analysis by adjusting group-level portfolio weights

Rebalance allocations across groups while keeping total portfolio value unchanged

Automatically reflect group-level changes in the underlying holdings

Compare adjusted portfolios to the original to evaluate the impact on performance and portfolio characteristics

Find it in the platform:

Navigate to the Portfolios tab from the top navigation

Go to the Reports tab, open a report and click the dropdown arrow next to the report name

Select Adjusted Portfolio Comparison

Choose By Groupings and select a grouping (e.g., GICS Sector, Industry, Region)

Adjust group-level portfolio weights; benchmark weights are displayed for reference

Click Update to view results

Optionally, Save the adjusted portfolios for continued analysis

Enhanced Folder Management

Users can access enhanced folder functionality to efficiently organize reports, layouts, and schedules – especially when managing many saved items.

Find it in the platform:

Navigate to the Portfolios tab from the top navigation

Go to Reports, Layouts, or Scheduled Reports

Click Edit, enable Select Multiple and select items using checkboxes

Choose Actions > Move to Folder

Move multiple reports, layouts, or schedules at once using multi-select

Organize Schedules into subfolders (e.g., Daily, Monthly, Quarterly, or by portfolio)

Simplify cleanup and reorganization without deleting saved artifacts

To return an item to its default location, select Reset Folder

When deleting a folder, choose the option to reset contained items instead of deleting them

MSCI Classifications

New MSCI classifications are now available for users as metrics or groupings in Portfolio Analytics reports, enabling richer geographic and market-level analysis.

New classifications available:

MSCI Geo Region Code: Analyze portfolios by major geographic regions such as Americas, EMEA, and APAC

MSCI Market: Classify holdings by market development level, including Developed, Emerging, and Frontier Markets

Find it in the platform:

Navigate to the Portfolios tab from the top navigation

Go to the Reports tab and open or create a report

Use the Grouping or Metrics menus

Select the desired MSCI classification

Note: Access to MSCI data requires an additional subscription, please contact your account team for details.

Credit Risk Pricing

In this release, we advanced Credit Risk Pricing to a GSAC v3-centered experience that brings greater structure, consistency, and discipline to transfer pricing analysis. A unified pricing interface presents inputs, outputs, and core measures on a single analytical surface, with parameter selection dynamically reflecting underlying curve coverage. The workflow supports immediate access to pricing and preserves access to established methodologies, ensuring continuity across both forward‑looking and historical analyses.

Consistent and Disciplined Credit Risk Pricing with GSAC v3

We enhanced the Credit Risk Pricing experience on the desktop, centered around GSAC v3. Pricing inputs, outputs, and visualizations are presented within a unified, structured layout for clearer configuration and interpretation of results. Risk‑free rates are represented consistently across currencies, and key pricing measures, including All‑in Yield and Z‑spread, are displayed in a consolidated view.

The workflow supports direct access to Credit Risk Pricing when applicable, while preserving the full scoring path for comprehensive analyses. Parameter selection dynamically reflects GSAC v3 curve coverage, guiding users toward supported sector, geography, and currency combinations.

Find it in the platform:

Search for and select a company in the top search

On the company’s profile, select Credit Risk Pricing from the left-hand navigation or choose Calculate Pricing from the Credit Risk Pricing widget

From the prompt, proceed using the latest available score or enter the Scoring workflow before reaching the Credit Risk Pricing page

Continuity for Transfer Pricing Across Credit Risk Pricing Methodologies

GSAC v3 now serves as the primary analytical surface for Credit Risk Pricing in the updated experience. For back‑testing, historical comparison, and established transfer pricing analysis, GSAC v2 and CYC methodologies remain accessible through the traditional Credit Risk Pricing interface. This structure separates forward‑looking analysis from historical methodologies while maintaining continuity across workflows.

Find it in the platform:

Search for and select a company in the top search

On the company’s tearsheet, select Credit Risk Pricing from the left-hand navigation or choose Calculate Pricing from the Credit Risk Pricing widget

From the prompt, proceed using the latest available score or enter the Scoring workflow before reaching the Credit Risk Pricing page

Select this link to redirect to the legacy interface, where data from CYC and GSAC v2 remains accessible

Credit Analytics in S&P Capital IQ Plug-In

In this release, we added EWS 1.0 to the S&P Capital IQ Plug‑In, enabling early warning signals for a company’s declining risk level.

Introducing EWS 1.0 in the S&P Capital IQ Plug-In

Users can now access six new EWS metrics in the S&P Capital IQ Plug‑In, helping them identify and predict potential credit risks or defaults before they materialize, and enabling proactive risk mitigation.

New metrics include:

IQ_EWS_SIGNAL

IQ_EWS_DAYS

IQ_EWS_PD_THRESHOLD

IQ_EWS_YOY_PD_CHANGE_PERCENT

IQ_EWS_DIMENSION1_STATUS

IQ_EWS_DIMENSION2_STATUS

Find it in the platform:

In Excel, launch S&P Capital IQ Plug-in and open Formula Builder

Navigate to the Early Warning Signal folder to access the new metrics

Note: These metrics support both prescore and OTF functionality